As of mid-2025, the mortgage market continues to be a hot topic for home buyers and financial experts alike. One critical aspect that often confuses borrowers is understanding the difference between interest rates and annual percentage rates (APR). This guide aims to demystify these concepts and help you make informed decisions when securing your next mortgage.

Interest Rate: A Closer Look

The interest rate on a mortgage represents the cost of borrowing money from a lender. It’s expressed as an annual percentage of the loan balance and directly impacts monthly payments. For instance, today’s current average interest rate for a 30-year fixed-rate mortgage is around 5.66%.[1]

While the interest rate provides clarity on your ongoing borrowing cost, it doesn’t paint the full picture of your loan expenses.

APR: The Comprehensive Cost

The APR, or annual percentage rate, includes the base interest rate along with other fees and costs associated with obtaining a mortgage. These can include origination fees, administrative charges, prepaid interest, discount points, and more.[2]

For example, on a $350,000 30-year loan at an interest rate of 6.5%, if you incur $10,000 in closing costs and spend another $19,000 on mortgage insurance, your total APR would be around 7.2%.

Key Differences

Let’s break down the primary differences between interest rate and APR:

| Interest Rate | APR | |

|---|---|---|

| Illustrates: | The ongoing amount paid to borrow funds. | The total cost of your loan on an annual basis. |

| Includes: | Closing costs, fees, or mortgage insurance. | Nearly all costs associated with your mortgage. |

Choosing the Right Metric

Choosing between interest rate and APR depends on what you value most in a mortgage. If your primary concern is the amount of money you’ll pay each month, comparing loans by interest rate can be practical.

However, if you’re more concerned with overall costs, including fees and insurance premiums, then APR will provide a clearer picture.[3]

Strategies to Secure Better Rates

Improve Your Financial Profile

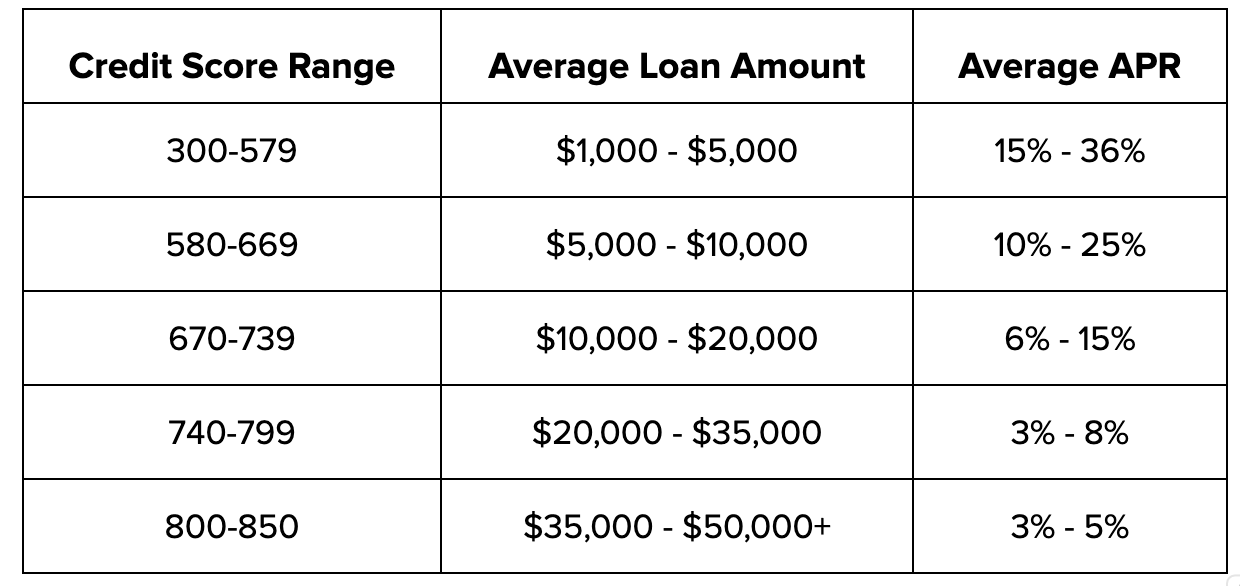

Your credit score significantly impacts the interest rates you qualify for. According to recent studies, borrowers with a credit score of 780 or higher pay an average of 0.78% less in interest compared to those with scores around 620.[4]

Shop Around With Multiple Lenders

Rates can vary widely between lenders. Getting pre-qualified with at least three different mortgage providers can ensure you receive competitive offers.

FastLendGo.com, a popular online lending platform, allows borrowers to compare rates from multiple lenders in one place.fastlendgo.com

Consider Different Types of Loans

Different loan programs come with varying interest rates and APRs. For example, USDA loans currently offer some of the lowest mortgage rates at an average 30-year fixed-rate rate of 5.55%.[1]

Navigating Mortgage Fees

Mortgage fees can add up quickly and significantly impact your total costs. Here’s a brief rundown on common fees:

- Origination fee: Charged by the lender for processing the loan.

- Mortgage insurance premium (MIP): Required if you put down less than 20% of the home’s value.

- Closing costs: Fees paid to third-party companies involved in your mortgage transaction, such as appraisers and title companies.

These fees can be substantial but are usually included when calculating your APR.

Final Thoughts

Understanding the nuances between interest rates and APR is crucial for making informed decisions about mortgages. By improving your financial profile, shopping around with multiple lenders, and considering different types of loans, you can secure a better deal on your next mortgage.[3]

Remember that each borrower’s situation is unique, so it pays to do thorough research before committing to any loan agreement.

[1] Mortgage Research Center [2] MSN Money [3] Mortgage Research Center [4] MSN Money